Program Lauches August 15, 2025

Florida’s Hometown Heroes Loan Program Relaunches August 18, 2025: Everything You Need to Know

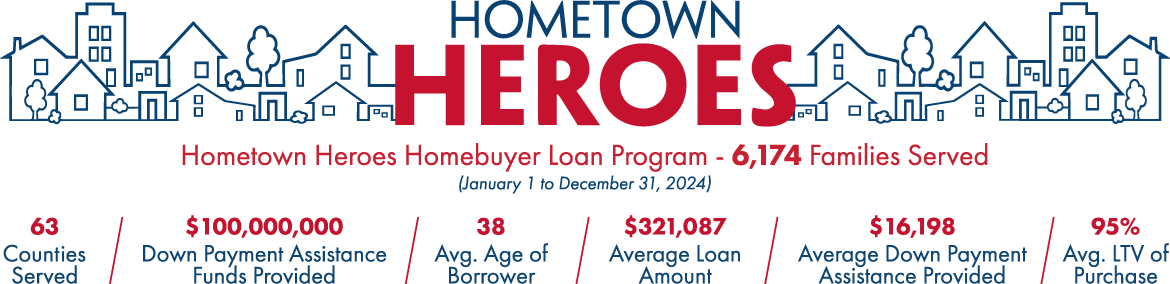

The Florida Hometown Heroes Program is scheduled to officially reopen on August 18, 2025, offering up to $35,000 in down payment and closing cost assistance for eligible first‑time homebuyers in designated public service and community roles. It’s a 0% interest, 30-year deferred second mortgage—with no monthly payment—due only at sale, refinance, or property transfer.

What’s New and Important for 2025

Florida Housing has allocated $50 million statewide for this year’s funding—about half of what was available in 2024—so demand is expected to outpace availability (in 2024 funds were exhausted in roughly 50 days). Though the fiscal year begins July 1, reservations and applications cannot be made until after the official launch following required Governor approval and lender training.

Who Qualifies?

Eligible Borrowers: Must be first-time homebuyers (no homeownership in the past three years)—veterans are exempt from this rule.

Minimum Credit Score: 640 required across FHA, VA, USDA, and conventional loan options (Make Florida Your Home).

Occupational Eligibility: Strictly limited in 2025 to specific full-time Florida‑based roles, including:

- Healthcare workers

- Educators

- First responders and public safety staff

- Court and public service personnel

- Child care workers

- Active military and full-time veterans working in state.

Employment Requirement: Must be employed full-time (35+ hours/week) with a Florida employer having a physical work location. Hybrid schedules may qualify with documentation; remote-only employees do not qualify.

Applicants must purchase a primary residence in the same Florida community where they work, designed to support local workforce stability.

Loan Structure

- Assistance Amount: Maximum of 5% of the first mortgage (minimum $10,000, up to $35,000), based on the primary loan amount .

- Loan Types Supported: FHA, VA, USDA, and conventional loans—with potential PMI reductions for conventional borrowers.

- Second Mortgage Terms: Fully deferred, non-forgivable, 0% interest; repayment required at sale, refinance, or deed transfer. No monthly payments.

Bond vs. TBA Program Options

Florida will offer two program structures:

- Bond Program: Lower interest rates; household income (including non-borrower adult members) counts toward the limits; lower income caps.

- TBA (To Be Announced) Program: Slightly higher income limits and interest rates; only borrowers’ incomes counted toward qualification.

Which path fits best depends on household income structure and the specific county’s income caps.

Income and Loan Limits

These vary by county based on 140–150% of Area Median Income (AMI).

For example:

- Palm Beach County: household income limit around $175,650.

- Broward County: approximately $172,950

- Miami-Dade County: $185,850.

Loan amount caps align with FHFA/Florida Housing conventional and FHA limits—but program guidelines provide terms for FHA, VA, USDA, and conventional loans.

Key Restrictions & Timelines

- New Construction: Closing must occur within 60 days of reservation, with a single 30-day extension allowed (maximum 90 days).

- Fee Caps: Broker fees capped ($0), lender fees capped ($1,700), no origination fees or discount points; documentary stamp and intangible tax exemptions save roughly $2,000–3,000 in closing costs.

Pre‑Approval Process: Lenders must have a fully executed purchase contract before locking in a loan or reservation—early eligibility verification is essential.

Other Requirements & Perks

Homebuyer Education: At least one borrower needs a certified course certificate (valid for two years)—veterans may be exempt.

Eligible Property Types: Single-family homes, condos, townhomes, or manufactured homes on permanent foundations.

Tax Savings: Exemptions from Florida documentary stamp tax and intangible tax can save thousands at closing.

What to Do Now

Check if your job is on the upcoming official eligible occupations list.

Speak with Tori Easterling early to begin pre-approval, verify documentation, and be ready to reserve funds as soon as applications open.

Review income caps for your county to make sure likelihood of qualifying (Palm Beach $175,650, but other counties differ).

Plan ahead for documentation—income verification, employment verification, credit score, and homebuyer education.

This program is a powerful, time-sensitive opportunity for community service professionals to access financial help with their home purchase. With official launch set for August 18 and limited funding, early preparation is key. Let me know if you'd like help organizing county limit sheets, occupation checklists, or informational summaries to share.